How to earn points and miles with fair to poor credit – The Points Guy

Update: Some offers mentioned below are no longer available. View the current offers here.

Travel rewards cards can be incredibly lucrative. Although the best sign-up bonuses or welcome offers often require high credit scores and unblemished borrowing histories, you can still get into the game even if your credit record isn’t sparkling. It doesn’t matter if you’re building credit for the first time or looking to rebuild, you have options.

Today, we’re going to look at how your credit score is calculated and discuss strategies for would-be award travelers with less-than-perfect credit. Let’s jump in.

Want more credit card news and advice from TPG? Sign up for our daily newsletter!

Credit score basics

Credit scores affect everything from interest rates on auto loans and your monthly mortgage payment to insurance rates and employee background checks when looking for a new job. The Fair Isaac Corporation (FICO) produces the most well-known personal credit rating, and lenders commonly use this number as the first metric to analyze your risk as a borrower.

The FICO score has a range of 300 (bad) to 850 (excellent)*. Generally speaking, having a higher score makes you a more attractive candidate for a loan. The average credit score is somewhere between 660 and 690. “Good” credit includes scores of 680 or above, and “poor” credit includes scores of about 620 and below. Top-tier or “excellent” credit starts around 740-750 and gives you a good chance of being approved for credit cards and other loans.

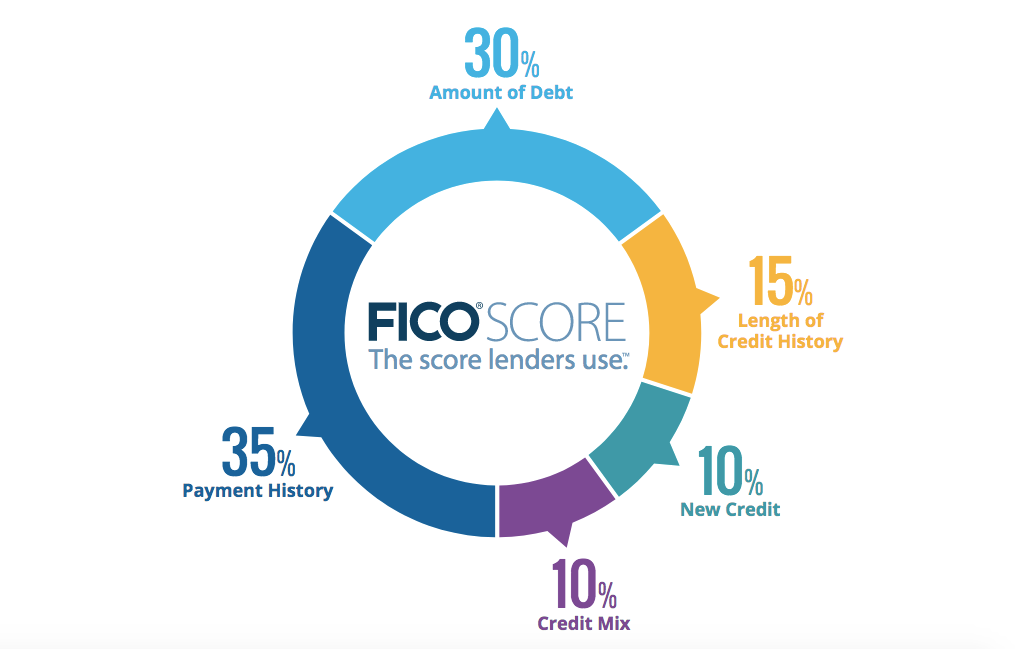

Your credit score is comprised of several different factors, as shown in the chart below:

The most critical factors are late or missed payments and your credit utilization (the ratio of how much credit you’re using to how much credit is available to you).

Negative remarks such as a late payment or accounts in collections stay on your credit report for seven years. That’s a long time to pay for a mistake and to have an obstacle to earning points and miles. Fortunately, negative remarks affect your score less and less as they age.

Daily Newsletter

Reward your inbox with the TPG Daily newsletter

Join over 700,000 readers for breaking news, in-depth guides and exclusive deals from TPG’s experts

People often mistakenly believe that you’ll automatically have a low score if you carry a lot of credit cards. However, each new account improves your credit utilization (so long as you’re not carrying significant balances), so having multiple lines of credit can have a net positive effect. There are other factors, and I’m not suggesting that you open a bunch of credit cards in order to improve your score. However, having multiple cards isn’t necessarily a bad thing.

Related: 6 things to do to improve your credit

A new type of FICO score

In 2019, FICO unveiled a new kind of numerical system called UltraFICO.

This is great for those who have a limited credit history or have had a financial hiccup in the past, as it allows lenders to look at other information from your checking and savings accounts to understand your approach to managing money.

For instance, the new score considers how long those accounts have been open and whether you have recurring monthly deposits to your savings account. As long as you display good behavior with your bank accounts, you should be able to climb into good or excellent credit score territory.

UltraFICO is an opt-in opportunity, and you have to be willing to give lenders access to information about your checking and savings accounts. However, if your credit score has been toward the bottom of the ladder — upper 500s to lower 600s — the new approach to gauging your creditworthiness can make all the difference to your financial life. If interested, go here to learn more about UltraFICO and sign up.

Related: How to improve your credit score in 2021

Protecting your credit

Travel rewards cards offer great opportunities to collect points and miles, and if you’re new to award travel, TPG’s beginner’s guide to getting started with credit cards can help.

However, your credit isn’t something you want to take lightly, so you should only pursue rewards cards if you’re well organized and have sound financial habits. Banks are wise; they offer these bonuses because they want to make money, and any interest or fees you pay can easily wipe out the value of your rewards. But if you hit your minimum spending requirements, pay off your balance on time each month without accruing interest and avoid other fees, you’ll come out ahead.

If you have less than “good” credit, it’s likely you’ve already missed payments, maxed out your limits or have judgments on your credit report. Making on-time payments from now on can help improve your score, but opening more credit cards to collect rewards is not a good way to manage your debt.

Nonetheless, if your credit score suffers from past mistakes that you have since corrected, or if your credit history is inadequate to put you in the upper tiers, you can still participate.

Related: What is a good credit score?

Rewards strategies for those with less-than-excellent credit

Poor credit (FICO score of 550 and below)

This group makes up less than 10% of all scores and if you land in this range, you probably won’t be approved for a points- or miles-earning credit card.

However, there’s a chance you may be approved for a secured credit card, which requires a cash deposit and works similarly to a credit card. Although this won’t earn you a ton of points and miles, it can help you build trust with lenders and creditworthiness for the future. You can use a secured credit card just as you’d use any other credit card.

Related: Trying to build your credit? Consider these secured credit cards

A good option for people in this boat is the no-annual-fee Capital One Platinum Secured Credit Card.

It’s one of the few secured credit cards that may extend you a credit line that’s greater than your security deposit. You will have to pay a minimum security deposit: $49, $99 or $200 for a $200 credit line. However, you can raise your initial credit line by the amount of your additional deposit, up to $1,000. You’ll be automatically considered for a higher credit line in as little as six months.

Related: Airline miles that are hardest to earn — and why you want them anyway

If you’ve applied for a secured card but keep getting denied, be aware that over-applying creates multiple credit inquiries, which can negatively impact you. If you simply can’t get approved, obtain a free copy of your credit report to determine precisely what is holding your score down.

If you aren’t approved for a secured card, you could pick up a rewards debit card. They are not as lucrative as they used to be, but some debit cards still earn points and miles.

For instance, the Delta SkyMiles® World Debit Card, issued by SunTrust, offers 5,000 bonus miles after your first PIN Point of Sale or signature-based purchase within the first 90 days. It earns 1 mile for every $2 spent on all PIN Point of Sale or signature-based purchases, with a cap of 4,000 miles per month. The card has a $95 annual fee and is only available to SunTrust Signature Advantage Checking Account holders.

Rewards debit cards are beneficial for expenses such as tax and mortgage payments that normally wouldn’t earn rewards without incurring a fee.

The information for the Delta SkyMiles® World Debit Card card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

Related: How to get started earning rewards with your first credit card

Subprime credit (FICO score of 550-620)

Roughly 15% of Americans fall within the “subprime” range. If you’re among them, your score is likely being affected by negative factors such as defaulted loans or credit cards, bankruptcy or foreclosure. You’ll probably need to wait until your score increases to get approved for the most rewarding cards, but there are other good options out there in the meantime.

For instance, you could start with a simple cash-back card such as the Capital One Quicksilver Cash Rewards Credit Card, which gives you a flat 1.5% cash back on all of your purchases.

The Capital One QuicksilverOne Cash Rewards Credit Card is helpful if you’re having trouble getting an adequate credit line since you can be automatically considered for a higher credit line in as little as six months. This card comes with a $39 annual fee.

Related: Capital One Quicksilver Cash Rewards card review

Acceptable credit (FICO score of 620-680)

A little less than 20% of Americans fit this description, and this is where you really start to have options. You most likely won’t be approved for premium travel rewards cards in this range, but you can still take advantage of some lucrative offers. Also, by managing your credit closely in this range, you can start to move toward a “good” or “excellent” rating, which can help you save considerably on future loans.

Your goal at this point is to build relationships with top card issuers by making payments on time and keeping your credit utilization low so that down the road, you have a better chance of being approved for more lucrative products. Two strong options at this level are the Chase Freedom Flex and Chase Freedom Unlimited cards.

Both of these cards carry no annual fees and can earn you significant Chase Ultimate Rewards points. When you have these cards alone, those points are no different than cash back. Still, if you also have an Ultimate Rewards-earning card such as the Chase Sapphire Preferred Card or the Ink Business Preferred Credit Card, you’ll be able to transfer your points to a variety of travel partners. TPG valuations peg Ultimate Rewards points at 2 cents apiece so you’ll effectively be doubling your return when you pair the cards.

Related: Maximize your wallet with the perfect quartet of Chase cards

The Freedom Flex rewards you with 5x points (5% cashback) per dollar on up to $1,500 in eligible spending on rotating quarterly bonus categories such as gas stations, grocery stores and department stores (activation required), 5x on Lyft rides (through March 2022), 5x on travel booked through Chase Ultimate Rewards, 3x on dining, 3x on drug stores and 1x on all other purchases.

Meanwhile, the Freedom Unlimited earns 1.5x points on all non-bonus spending. Both cards offer new cardholders a $200 (20,000-point) sign-up bonus after spending $500 on purchases in the first three months from account opening.

If you prefer a card with no annual fee that allows you to transfer your points to travel partners without having to get another card, there’s The Amex EveryDay® Credit Card from American Express. It earns 2x points at U.S. supermarkets for up to $6,000 a year in purchases and 1 point per dollar after that and elsewhere. New cardholders get 10,000 Membership Rewards points after spending $1,000 in purchases within the first three months of account opening.

The information for the Amex EveryDay® Credit Card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

It’ll likely take a while until you can book a coveted redemption such as Cathay Pacific first class, but you’ll be off to a good start.

Related: The top credit cards with 0% intro APR

Good credit (FICO score of 680-740)

If you have good credit, you’re among the 25% of Americans who fall into this range, which allows you to really start using your credit score to your advantage. Although all scores within this range are considered “good” and are only separated by 60 points, a 740 FICO score can command much lower borrowing rates. Still, a 680 score puts you within reach of some of the best credit cards out there.

A terrific option to start with is the Chase Sapphire Preferred Card, which offers a sign-up bonus of 80,000 bonus points after you spend $4,000 on purchases in the first three months of account opening. Those 80,000 points are worth a whopping $1,600, according to TPG’s current valuations.

With this card, you’ll earn 5 points per dollar spent on travel when booked through the Chase Ultimate Rewards portal, 3 points per dollar on dining purchases,3x on select streaming services, 3x points on online grocery purchases (excluding Target and Walmart), 2x points on all other travel, and 1 point per dollar spent everywhere else. You’ll also get perks, including a complimentary DoorDash DashPass membership (activation required by March 31, 2022), primary car rental coverage, trip delay protection and no foreign transaction fees. This card has a $95 annual fee. Read more about the Chase Sapphire Preferred Card.

Related: What credit score do you need to get the Chase Sapphire Preferred card?

Another strong card option for people in this credit range is the American Express® Gold Card.

Its 60,000-point welcome offer after spending $4,000 on purchases in the first six months of card membership isn’t as exciting, but it gets you 4x points per dollar spent on dining at restaurants and U.S. supermarkets (on up to $25,000 per calendar year at U.S. supermarkets; then 1x), 3x points per dollar on flights purchased directly with the airline or at Amex Travel, and 1x point per dollar on other purchases.

That equates to a stellar 8% back on dining at restaurants and U.S. supermarkets and 6% on airfare, according to TPG valuations. The card’s $250 annual fee (see rates and fees) is higher than that of the Chase Sapphire Preferred, but it also comes with more perks, such as annual dining credits (up to $120) per calendar year and annual up to $120 in U.S. Uber Cash annually ($10 monthly credits) per calendar year. Card must be added to Uber app to receive Uber Cash benefit. Enrollment required for select benefits.

You may have noticed a large jump in the spending requirements to earn the bonus for these cards compared to those mentioned earlier. If you’re climbing back from past credit problems, the last thing you need to do is to spend $4,000 that you can’t pay back on time. However, if you can meet the spending requirements responsibly, the welcome offers speak for themselves.

Related: 11 ways to meet credit card bonus minimum spending requirements

Excellent credit (FICO score of 740-850)

Between 35-40% of Americans have a FICO score of more than 740. In this range, you’re most likely to be approved for the best products out there, including all of the cards on TPG’s list of the best travel rewards credit cards. However, even if you have excellent credit, the cards mentioned earlier can be useful to have in your wallet, so don’t discount them.

There’s also the Citi Premier® Card, which currently comes with a sign-up bonus of 60,000 ThankYou points after you spend $4,000 in purchases within the first three months of account opening (see rates and fees). TPG values ThankYou Points at 1.8 cents apiece, so the bonus alone is worth $1,080. With this card, you’ll earn a solid 3x points per dollar spent at hotels, air travel, supermarkets, restaurants, and at gas stations. The card has a $95 annual fee.

Related: The best elevated credit card offers

Bottom line

The travel rewards game isn’t just for those with sterling credit. In fact, there are great opportunities to select cards that, when managed correctly, can help rebuild damaged credit. Remember not to overextend yourself trying to meet spending requirements and to practice sound financial habits. After all, the first commandment for rewards credit cards is to pay your balance off in full each month.

Even if you don’t currently qualify for the best offers, you can become eligible with time and careful management. The benefits of improving your credit score extend beyond the points and miles you earn, but those rewards make doing so a lot more fun.

If your application is initially denied, that decision isn’t necessarily final. Many people have had success by calling the reconsideration line and explaining their situation. Sometimes your applications will be approved or denied instantly by a computer algorithm, but often the decision to offer you credit lies with a human. If you’re not approved instantly, give the card issuer a call and explain why you’ll be a valuable customer.

Additional reporting by Chris Dong.

For rates and fees of the Amex Gold card, click here.

New to the points and miles game? Check out our beginner’s guide for everything you need to know to get started!

*The Points Guy credit ranges are derived from FICO® Score 8, which is one of many different types of credit scores. If you apply for a credit card, the lender may use a different credit score when considering your application for credit.

RELATED VIDEO: